The Promise and Perils of Smart TV Gaming in US

Source: https://www.amazongamestudios.com/en-us/news/articles/new-amazon-luna#ags-MediaPopup

Source: Amazon Luna

Earlier this month, Netflix and Amazon both revealed plans to pivot their gaming services toward casual smart TV gaming. Netflix is adding five new party games to a new Games tab in its TV app this holiday season, while Amazon is relaunching Luna to center around a new “GameNight” party game collection later this year.

They aren’t the only companies making waves in the TV gaming market, which until recently has been a quiet, poorly understood niche within the games industry. OEMs like Samsung and Roku are investing in the space alongside smaller streaming services, while startups like Volley are raising tens of millions to pursue the opportunity.

What is driving the rise of activity and investment in TV gaming? Amazon, Netflix, and others have lofty visions — but will it be enough to transform the moribund subsector into gaming’s next big growth story?

The Evolution of TV Gaming

“Smart” TVs — meaning televisions that connect to the Internet — hit the market in the late 2000s, and Samsung released the first TV app store in 2010, less than two years after Apple launched its game-changing App Store on iOS. As the smart TV market grew, the likes of LG, Roku, and eventually Amazon and Google pushed TV app stores, full of mostly video streaming apps — but also games. These games were, by and large, low quality ports of web games or early mobile titles, and even today the Games section of most TV app stores is populated with this type of content: extremely basic, arcade-style gameplay reminiscent of defunct Flash portals.

Source: https://channelstore.roku.com/browse/games

A screenshot from Roku’s app store in 2025. Source: Roku

While the gaming content on TV app stores has changed little in the past fifteen years, by the early 2020s the emergence of cloud gaming initiated the second era of TV-based gaming, capturing the attention of big tech and startups. Google Stadia, Nvidia GeForce Now, Amazon Luna, Xbox, and smaller firms like Boosteroid, Utomik, and Blacknut all launched smart TV apps from 2021 to 2023. TV OEMs also launched products like Samsung Gaming Hub and LG Gaming Shelf to merchandise these third-party services and the games within them.

In the years since, it became apparent that cloud gaming would not unlock smart TVs as a new platform for games. Coupled with the high operating costs of cloud gaming, these services suffer from a limited addressable market. People who enjoy console-style games enough to own a compatible controller, connect it to their TV, and subscribe to a service, but who don’t like gaming enough to already own or buy a console don’t exist in high numbers.

Source: https://news.samsung.com/us/samsung-gaming-hub-portfolio-expands-to-nearly-3000-games-with-launch-of-antstream-arcade-and-blacknut/

A screenshot of Samsung Gaming Hub merchandising console games to be played with cloud gaming subscription services. Source: Samsung

TV Gaming’s New Era

Netflix and Amazon’s recent announcements indicate that TV gaming has officially entered its third era. Casual games made specifically for the TV form factor are the dominant content type on which a plethora of companies have pinned their hopes for the space. While this month’s splashy announcements mark a high-profile pivot for Amazon and other firms, this is actually the culmination of a years-long shift away from console-style cloud gaming and towards this new game format.

Return Entertainment, led by Rovio veterans, raised $6M in 2022 to build games specifically for TVs, using phones as controllers (as simple as scanning a QR code on the TV to begin) while still relying on cloud technology. Volley, a San Francisco startup, began creating voice games for smart speakers in 2016, but raised $55M in 2024 to double down on smart TVs as its biggest growth opportunity.

Source: https://www.volleygames.com/post/volley-launches-on-amazon-fire-tv-with-jeopardy

Volley’s voice-based Jeopardy game being played on an Amazon Fire TV. Source: Volley

Both startups received funding from Samsung, which was simultaneously developing its own portfolio of minigames for its TVs, unveiled earlier this year. Meanwhile, developers like Play.Works and Magicyard were honing their expertise in specially developed smart TV games and signing partnerships with Paramount and DISH Network (Magicyard was quietly acquired by Volley in 2024). Roku, too, has been actively scouting for new casual games built for TVs in recent years.

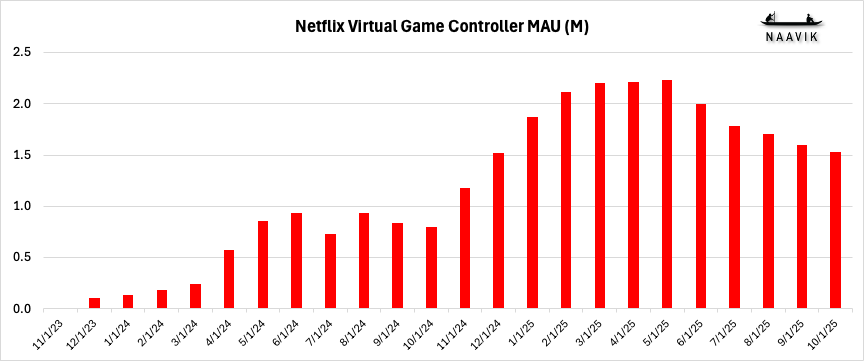

Early results from this era of TV gaming indicate promising, if early, results. Volley reports over 5M monthly active users across its smart speaker and TV portfolio, while Play.Works boasts it reaches over 400M households with “60% weekly retention.” Netflix’s current (beta) portfolio of cloud games, which requires use of a dedicated mobile app for play on either TV or a PC, includes OXENFREE and the recent Happy Gilmore game. According to Sensor Tower, the required mobile app currently has about 1.5M monthly active users.

Source: https://sensortower.com/

Source: Sensor Tower

Netflix, Amazon, and Volley are focused on subscriptions, while Samsung, Play.Works, and others such as Zone-ify and Future Today are monetizing via ads. Despite their varying business models, these companies are finally grasping what makes TV unique as a potential gaming platform and building games that embrace the form factor. However, crafting content specifically for TVs only solves one of many challenges that remain if TVs are ever to become a mainstream gaming platform.

Source: https://news.samsung.com/us/samsung-expands-game-offering-and-provides-more-ways-to-play-leading-up-to-summer-game-fest-2024/

Return Entertainment has published Rivals Arena, a card battler, on Samsung and Amazon Fire TV. Source: Samsung

Why TV Gaming Has Failed So Far

This pivot towards developing games natively for TVs, rather than porting or streaming existing games, reflects the many challenges that continue to plague TV gaming across many categories:

Hardware and User Input

As devices, TVs have significantly less processing power than mobile phones because they are designed for simpler, static tasks like video decoding and upscaling while running only a handful of apps. A typical TV may have 1-3 GB of RAM, while even low-spec phones usually have at least 8 GB. This reduces the responsiveness of user input on a TV, a critical factor for games. Many companies bet on cloud gaming as a workaround but then incur the high variable costs of game streaming.

While newer TV models may address these hardware limitations (or may not – Google reduced the RAM requirements for Android TVs last year to just 1GB), consumers do not replace their TVs very often, meaning that any hardware improvements take several years to reach a critical mass of users.

TV controllers are also highly unoptimized for gaming; they are often cheaply made, uncomfortable to hold for long periods of time, and designed to navigate basic menus and functions, not respond to even moderately complex gameplay inputs. While nearly all TVs support Bluetooth connections with console controllers, most users do not own controllers or will not bother to connect them. Using phones as virtual controllers (like Amazon and Netflix), or relying on voice input as Volley does, sidestep these issues but present their own challenges.

Distribution and Monetization

While TV app stores have existed for many years, they are clunky to navigate and often not intuitively accessible from TV home screens. Recommendations, search, editorial, lists — features taken for granted on mobile, PC, and console storefronts — are often absent in TV app stores. There are also few reasons for a user to visit their TV’s app store, as most common apps (Netflix, Disney+, YouTube, etc.) are already preinstalled on the TV and users rarely need to download new apps to access popular content.

TV operating systems also have limited monetization functionality. Native support for purchasing apps or making in-app purchases on devices from Samsung, LG, Vizio, Roku, and many other OEMs is entirely or nearly absent — or at best far more limited than any gaming storefront. Users also rarely have payment information associated with their TV accounts, if they are even signed in to one, adding significant friction to any checkout process if one is even possible. For nearly all apps, TVs are fundamentally set up for users to simply log into a subscription service they signed up for on a phone or laptop.

Ad monetization is a potential (but not yet reliable) bright spot, as many TV OEMs have scaled ads businesses for their free ad-supported streaming services (e.g., The Roku Channel, Samsung TV Plus). But bridging the gap between TV ad sales and gaming ad monetization remains a challenge yet to be overcome.

Market Fragmentation

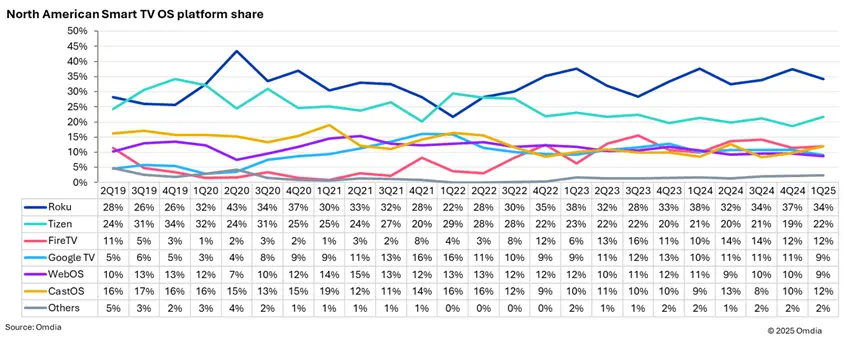

Compounding these challenges is the highly fragmented nature of the TV market. Not only are the hardware, OS, distribution, and monetization options on TVs already challenging for game developers to work with, but each TV OS is very different and none have a truly commanding market share. Even with a single OS, there can be significant fragmentation amongst hardware models and OS versions.

Source: https://omdia.tech.informa.com/blogs/2025/july/the-smart-tv-os-shakeup-amazon-walmart-and-the-coming-age-of-shoppable-media

Roku is the leading TV OS in North America, but Tizen (Samsung) is the leader globally. Source: Omdia

This makes it difficult to scale and maintain gaming content across multiple systems, as each new OS to port a game requires significant development resources. Play.Works’ ability to distribute games across nearly all types of TVs would be taken for granted on mobile or PC, but it is an incredible feat on TVs that is possible only thanks to its significant investment in a proprietary technology and ad monetization platform. Volley, meanwhile, is using its Series C funding to build “core technology infrastructure to enable a ‘write once, run everywhere‘ development environment as we expand our games to additional OSs and platforms.” These capabilities are competitive advantages for these companies, but they also demonstrate the significant friction developers have in scaling across such a fragmented market.

In many ways, smart TVs are at the same stage that PCs were before Steam or mobile gaming was before the iPhone — ubiquitous general-purpose computers with a fragmented ecosystem and few unifying standards.

Player Behavior

Lastly, even if a company can overcome all these obstacles to building, widely distributing, and monetizing a TV game, they still face additional hurdles. While all games compete for the limited time a user can spend playing games, TV games face an even steeper uphill battle.

Users do not yet think of their smart TVs when they want to play games. They instinctively reach for their phone, PC, or console instead, reinforcing those habits each time they do so. And when they do turn on their smart TV, they almost always looking for video content where they can vanish into a new show for hours with a single press of the Play button.

Competition against other games and other forms of media is not unique to TV games. For now, however, TV games are disadvantaged against both — even before the relative quality and fun of these new, unproven TV games is taken into account.

The Party Games Dilemma

To this end, Netflix, Amazon, and others have leaned into the unique factors about the TV that make it more appealing than alternatives. Local multiplayer party games with virtual controllers on players’ phones, monetized via existing subscriptions, are what both Netflix and Amazon are launching this holiday season. This type of content makes the most of the big screen, living room format while avoiding some of the challenges inherent to TV game development.

Source: https://www.aboutamazon.com/news/entertainment/amazon-luna-redesign-gamenight-prime

Amazon Luna’s new GameNight collection centers on the AI-powered Courtroom Chaos party game featuring Snoop Dogg, but includes other classic party games like Exploding Kittens and Clue. Source: Amazon

Yet even this choice carries risk. Both companies hope that families gathering for the holidays will try out these games (as many families already do with Jackbox Games or traditional board or card games) and want to keep playing them into the new year. While leveraging seasonality is a smart launch strategy, local multiplayer party games are rarely, if ever, played with any regularity. While the occasional family or group of friends may have a weekly game night, frequency of gameplay sessions in this genre is low compared to singleplayer or online multiplayer games. Games that can only be played when people gather together in the same place are simply not played very often, at least among the mass market audience that Netflix and Amazon are targeting.

Assuming the goal of both Amazon and Netflix’s new party games is to boost subscriber retention, it remains to be seen whether party games that only get played occasionally will meaningfully affect customer loyalty. Of course, party games on TV are just a part of each company’s broader gaming strategy. Netflix, for example, has described party games as just one of four categories of gaming content it is prioritizing under new President of Games Alain Tascan, along with kids games, mainstream (presumably licensed) titles like the Grand Theft Auto Trilogy, and “immersive” games based on its IP, such as Squid Game: Unleashed.

Source: https://about.netflix.com/en/news/level-up-your-holidays-with-party-games-coming-to-netflix-on-tv

The five party games Netflix is launching for TVs later in 2025. Source: Netflix

Looking Ahead

Despite the challenges facing the category today, the long-term potential of smart TV gaming is enormous. Nearly every household already owns multiple large, internet-connected screens that provide a uniquely communal and immersive entertainment experience, distinct from phones, tablets, and PCs. The total addressable market is massive — virtually every connected TV is a potential gaming device — but the many technical and market barriers currently constrain its uptake.

Of the companies competing in this space, Netflix is currently best positioned. It has 300M global subscribers, most of which (at least in the US and Northern Europe) primarily interact with it via its smart TV app, giving it a massive potential audience for its new games. For many people, Netflix is the default app to open when turning on the TV, and now it will feature games. Amazon, on the other hand, has 200M global Prime subscribers; all of these users (with certain regional limitations) have access to Luna, but unlike Netflix, Luna is a separate app that most users aren’t aware of, let alone open out of habit.

OEMs like Samsung, LG, and Roku have the advantage of controlling app distribution, but even for market leaders, their reach is still limited to their install bases within a highly fragmented market. This puts their gaming efforts at a mass-market disadvantage to cross-platform services like Netflix or even pure-play TV gaming publishers like Volley, Play.Works, or Return Entertainment. These publishers are the most focused and innovative firms in this nascent space, yet they are also the most constrained by the myriad challenges of TV game development.

Many things must change for this market to reach its potential, but as the third wave of TV gaming accelerates, its momentum may force the ecosystem shifts that are needed. Party games themselves have limited potential, but with the weight of Amazon and Netflix behind them, they might be the most effective beachhead for TV gaming to break through and gain its first sizable audience. Beyond that, distribution and monetization across devices and operating systems must be solved to enable more complex and diverse gameplay in order to fully open this opportunity for developers, publishers, and players.

Source:https://naavik.co/digest/the-promise-and-perils-of-smart-tv-gaming/

Hot News

- A New Chapter for Chinese Animation: Integration of Digital Intelligence and Global Exchange – The 22nd China International Cartoon & Animation Festival Concludes Successfully

- European Gaming Industry Roundup 2026: Revamped Exhibition Layout & Booming Market Heat Usher in a Diversified New Landscape

- Star Wars: Galactic Racer™ explores bitter rivalries at Summer Game Fest

- Japanese Entertainment Giant FuRyu Establishes Wholly-Owned Subsidiary in Guangzhou to Deepen China ACG Market Layout

- Fire Emblem: Fortune’s Weave Sets Global Launch for September 17, Exclusive to Nintendo Switch 2

- Where West Lake Inspires New Visions: Integration of Technology and Arts Forges a New Industrial Ecosystem

- No Mobile-Exclusive Titles Featured at Summer Game Fest: Deepening Industry Divisions Signal a New Refined Independent Growth Era for Mobile Games

- Quiet Express: Cabin 909 Confirmed for Release in 2027