Has Esports Spring Officially Arrived?

Source: https://www.forbes.com/sites/ibm/2020/01/08/how-esports-are-fueling-the-data-economy/

Source: Forbes

It wasn’t that long ago when esports was heralded as the future of entertainment. Twitch metrics exploded. Venture capital flowed. Franchises in leagues like the Overwatch League (OWL) and Call of Duty League (CDL) were selling for tens of millions of dollars. Esports organizations became talent agencies, streetwear brands, and streaming collectives. At its peak, some even speculated that esports viewership would consistently surpass the largest sports leagues.

And then the bubble burst.

From 2021 to 2023, the entire esports industry began to grapple with a reality that wasn’t as rosy as previous aspirations. Revenue expectations failed to materialize, investor patience and financing ran dry, and the business models underpinning many organizations proved unsustainable.

Now, in mid-2025, the industry is reemerging. But is this the start of a new, healthier growth cycle, or will history repeat itself? Let’s unpack what led to the winter, what’s happening today, and whether esports’ spring is truly in bloom.

A Brief History of Esports’ Winter

Between 2015 and 2020, esports entered a hype supercycle. Viewership was hot, but revenue didn’t keep pace despite many investors’ original belief that esports would monetize similarly to traditional sports.

Sadly, they were wrong. Unlike sports leagues, which generate billions through media rights, esports has largely moved away from exclusive streaming rights, which reduces media rights revenue for teams via leagues. In-person ticket sales don’t resonate the same way for digital sports compared to physical sports; merchandise sales are generally more limited (choosing which team to be a fan of can be harder); and teams can’t rely on prize pools, given the competitive market. That leaves sponsorships as the primary revenue source, which have been shown to be volatile and insufficient to support ballooning costs. Crypto volatility and the fall of FTX was a notable factor of this, too, from a sponsorship lens.

The pandemic initially buoyed viewership, but the structural problems remained. Team valuations collapsed. The Overwatch League dissolved. FaZe Clan’s $725M SPAC turned into a $17M acquisition. TSM, CLG, and others sold their franchise slots in major leagues. Layoffs swept the industry. And by 2023, the term “esports winter” became the shorthand for a necessary yet painful reset.

The Present

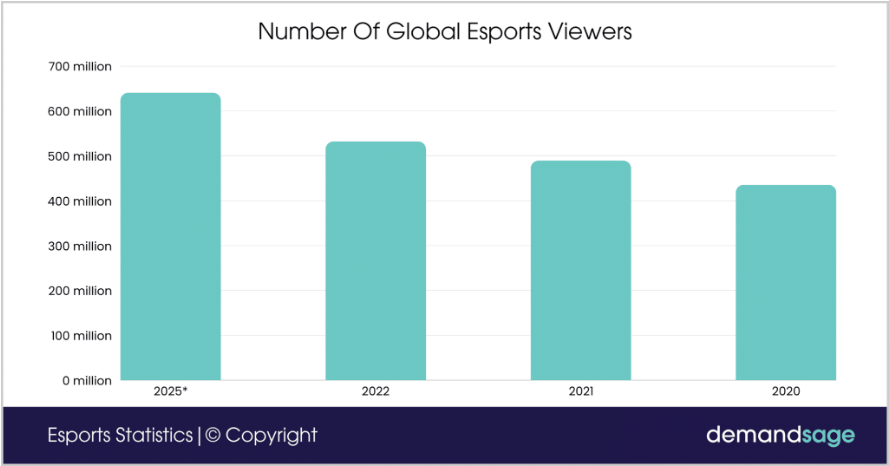

Source: https://www.demandsage.com/esports-statistics/

Source: demandsage

Despite the downturn, esports obviously didn’t die; it normalized. Viewership remains large, with over 600M estimated viewers expected for 2025. Only half of that number is dedicated fans, and over half of this engagement is from Asia. But however you slice it — or trust the numbers — the industry has been fundamentally reshaped, and there are multiple dynamics at play.

Publishers Hold Significant Power

Game publishers have always owned a game’s IP, and their control is clearer than ever. Most publishers continue to decide if and how esports exists for their titles.

Riot Games continues to centrally operate League of Legends and Valorant leagues, experimenting with revenue sharing, co-streaming, and regional partnership models. Valve takes a laissez-faire approach to Dota 2 and Counter-Strike 2 (CS2), relying on third-party tournament operators (namely ESL FACEIT Group). Activision Blizzard shuttered OWL and CDL’s original franchise models, favoring simpler competitive formats. And other companies like EA continue to keep a tight control over the esports operations of their franchises.

This vertical integration means esports usually exists more as a marketing and player engagement tool than a profit center. That makes leagues susceptible to publisher priorities, and that means the financial success of teams across the ecosystem is not the ultimate priority.

Teams Are Evolving and Refocusing

The traditional esports team business model (win trophies, sell sponsorships) proved mostly insufficient. In response, many organizations have pivoted.

Many rosters have shrunk, with teams exiting low-ROI games and focusing on fewer titles with more discipline (like FaZe Clan dropping many streamers and games, and focusing mostly on CoD and CS2).

Teams have diversified into content and apparel — some to an extreme: 100 Thieves also launched an energy drink business and acquired a keyboard business. This was designed to win over more fans and better cross-sell, but doing so with limited resources proved challenging and led to refocusing priorities across the industry.

Similarly, we’ve seen more creator-owned organizations. Streamers like MoistCr1TiKaL (who created Moist Esports, which later merged into Shopify Rebellion) and Disguised Toast (who created Disguised) are subsidizing competitive teams for content and community-building purposes. These organizations are small but culturally relevant.

Yet profitability remains elusive for most. Sponsorships still dominate revenue, and there’s still no easy answer for better monetizing fandom. Most teams lack a diversified income, and it’s brutally hard to build any sustainable sources of competitive advantage. It might be fun, but it’s frankly not a great place to be in the value chain.

Saudi Arabia, the New Esports Superpower

Once venture capital dried up, Saudi Arabia’s Public Investment Fund (PIF) emerged as the biggest financial force in global esports. With its Saudi Vision 2030, Saudi Arabia is looking to reinvest over a trillion dollars of oil money back into its economy to grow and modernize the kingdom in new ways — and gaming/esports alone has at least $38B earmarked.

Savvy Games Group (fully funded by the PIF) acquired ESL and FACEIT and merged them into ESL FACEIT Group (EFG). And EFG is in as strong of a position as it gets. Not only has it been consolidating the event space (for games like Counter-Strike), but it’s able to better leverage its audience to cross-sell services like FACEIT Plus, which provides premium matchmaking services and advanced statistics to players. Consolidating around event organization and services for passionate players is a unique and rare way to build competitive advantage in the esports space. (Check out our interview from a couple years ago with the co-CEOs to learn more.)

Additionally, Saudi Arabia has launched and financially backed the Esports World Cup (EWC), which is currently ongoing. The EWC is a two-month tournament, hosted in Riyadh, that spans 25 games and 2,000 players across 200 teams — a tremendous organizational accomplishment. It is also led by ESL Co-founder Ralf Reichert.

Source: Esports World Cup Foundation

For the current event (which is the second annual installment), the EWC is boasting a $70M prize pool and $20M in team subsidies (via the Club Partner Program) — all bankrolled by Saudi Arabia. (And this isn’t accounting for the costs of hosting people, the venues, the opening ceremony, etc.) Between ticket sales (100K-plus so far) and sponsorships, the event will likely earn tens of millions in revenue, but it won’t be profitable. It’s a subsidized good for the industry and for Saudi Arabia.

Some key sponsors of the event are Saudi government-owned businesses like Saudi Aramco or fully aligned national companies like Dr. Sulaiman Al Habib Medical Group. Importantly, this latter entity is a nonprofit that’s far more interested in growing Saudi Arabia’s influence and growth than making immediate money.

All of this is great as long as the Saudi government doesn’t overinvest and then decide to stop. Many teams might rely on growing prize pools and subsidies to help maintain their businesses, and that creates a reliance risk. Overinvestment here wouldn’t be as dire as the VC-backed hype cycle from years ago, but it should still be avoided. And it’s naturally fair to be cautious about the long-term sustainability of something that rational, profit-seeking money would not fund.

Also, while the event is well organized in Riyadh (I visited and enjoyed my time last week), in order to reach more people, the tournament should consider moving outside of Riyadh in future years, but it’s unclear if the Saudi backers would approve that. We also chatted with COO Mike McCabe on the podcast recently about EWC’s ambitions, so check that out for more details.

Asia Continues to Lead

Source: https://www.globaltimes.cn/page/202111/1238353.shtml

Source: Global Times

China remains the world’s largest esports market by revenue. Mobile titles like Honor of Kings, PUBG Mobile, Free Fire, and Mobile Legends: Bang Bang dominate in East and Southeast Asia. In these regions, mobile esports viewership regularly outpaces PC/console titles, with tournament ecosystems drawing tens of millions of viewers per event.

Importantly, Asian esports teams tend to be on stronger financial footing than their Western counterparts. Many are owned or backed by major publishers and tech companies. For example, Edward Gaming is supported by Tencent, and Weibo Gaming is owned by social media giant Weibo. These teams benefit from more integrated ecosystems, shared infrastructure, and financial safety nets. Tournament operators like Hero Esports (formerly VSPN, the largest in Asia), which are also backed by Tencent and Savvy Games Group (another example of Saudi Arabia investing in esports), not only run events but support affiliated teams with greater scale and margin.

Compared to Western teams — which historically operated as standalone, VC-backed entities reliant on volatile sponsorship revenue — Asian teams are often more vertically integrated. While most Western organizations are still unprofitable or break even at best, many Asian teams enjoy stronger institutional support, diversified income streams, and longer-term backing.

Government support also plays a role. Esports is now a medal event at the Asian Games, and countries like China and South Korea actively fund esports infrastructure and training programs. Even amid tough regulations (like China’s gaming time limits for minors), esports remains culturally embedded and institutionally reinforced.

While the West retrenched, the East continued to build. Asia’s esports ecosystem is not just larger; it’s proven to be more sustainable.

The Future

Esports winter has ended, and spring is here, but it doesn’t look like what the industry once imagined. Instead of explosive valuations and exponential growth, the future of esports is being built around more rational economics, grounded execution, and less hyperbolic bets.

Across the industry, we continue to see consolidation and right-sizing. Teams have narrowed their focus, cut unprofitable games, and explored revenue streams like digital items, creator integrations, and premium content. Tournament organizers are hosting fewer but more compelling events. And publishers are experimenting with monetization schemes that align more directly with team incentives, such as revenue-sharing through in-game cosmetics.

Fan monetization still has much to prove, but signs point in the better directions. Riot’s Valorant Champions skin generated over $16M in 2022, with a substantial cut going to participating teams. More organizations are exploring merchandise, memberships, and ways to create value beyond just match results.

Geographically, the industry is bifurcating. Asia is pulling ahead — financially, culturally, and structurally — with publisher-owned teams, national investments, and mobile-first fandoms. Western groups, still emerging from a painful correction, have begun to professionalize, but they remain hampered by fragile business models and inconsistent revenue. The gap may continue to widen.

Meanwhile, new risk vectors are emerging. Sovereign wealth funding is propping up parts of the industry, and that may not last forever. Publishers still hold outsized power, and their shifting priorities can reshape the competitive landscape overnight. Besides, who knows how else the industry might change from here. Will the Roblox generation of younger players care about esports the same way? Will the seismic AI technology shift change the way masses engage with and compete in games? Will today’s biggest esports continue to last the test of time in an industry filled with change?

Only time will tell.

Still, there is more cause for optimism than skepticism. The era of irrational exuberance is over, but in its place is a sturdier foundation: growing audiences, more focused operators, and a slowly expanding tool kit for monetization. Esports likely won’t become the next NFL, but it doesn’t have to for esports spring to be exciting, durable, and engaging for fans and teams worldwide.

Written by Aaron Bush, Naavik Managing Partner, original link:https://naavik.co/digest/has-esports-spring-officially-arrived/

熱門頭條新聞

- Zoland Animation Sets Benchmark with “IP+Tech+Cultural Tourism” Integrated Model;

- New Action RPG Guardian Maiden Announced for Worldwide Release on PC and Mobile

- Alpha Nomos Brings Its Beat-Synced Combat to PlayStation 5 & Xbox X/S

- Crystal of Atlan Summer Fest Returns With New Content to Explore in Seaside Reverie

- A cozy flower garden in the corner of your screen: BuGarden out 22nd September!

- Record-Breaking Malaysian Animation Papa Zola The Movie Kicks Off Major Global Rollout; Authentic Local Storytelling Captures Worldwide Attention

- Evolution of Game Monetization Maps Global Investment Trends;

- Human Fall Flat Celebrates 10 Year Anniversary Alongside 60 Million Players