2025 Global Top-Grossing New Mobile Games Report Released: Asian Developers Continue to Lead, Hybrid Gameplay and Established IPs Serve as Dual Growth Engines

Recently, industry data firm AppMagic released the 2025 annual report on the revenue ranking of new global mobile games (covering in-app purchase revenue from iOS and Google Play stores, excluding ad monetization and third-party Android channels). The data indicates that although no single “super hit” with revenue exceeding ten billion dollars emerged during the year, the market exhibited a more balanced and diverse competitive landscape. Asian developers dominated the top 15, leveraging mature IP operations and hybrid gameplay innovations, with Chinese companies performing particularly strongly.

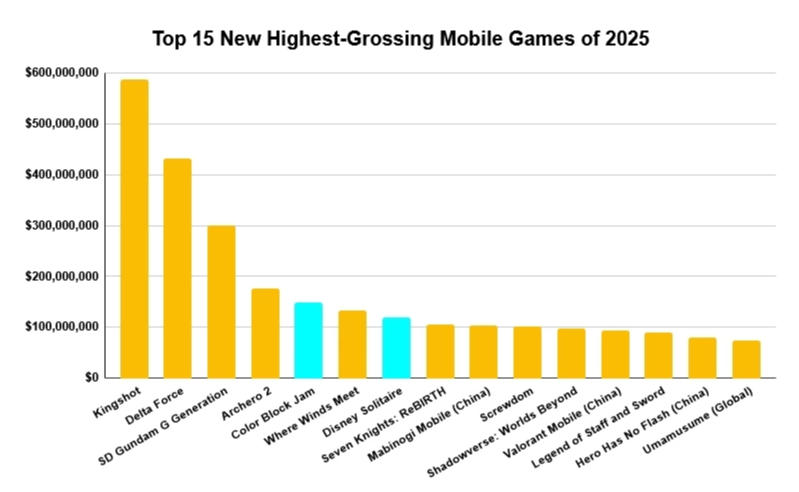

Market Overview: Total Revenue of Top New Titles Contracts, But Distribution Becomes More Balanced

From January to November 2025, global mobile game player spending in mainstream app stores totaled $72.6 billion, a slight 1% increase compared to the same period last year. However, the revenue-generating power of annual new releases showed some adjustment: the total revenue of the top ten new games was approximately $2.2 billion, down about 27% from the $3.0 billion of the top ten in the same period of 2024.

A positive change is the slightly less concentrated revenue distribution among top new releases in 2025. All new games that made it into the top ten revenue ranking surpassed the $100 million milestone in cumulative player spending, and all were released in the first half of the year. This contrasts with last year’s situation which relied on hits launched in the second half to drive the rankings.

Regional Landscape: Asia’s Dominance Remains Firm, Chinese Developers Secure Seven Spots

Asia, particularly China, continues to demonstrate its strong competitiveness in the mobile game market. Among the 15 highest-grossing new games, seven were developed by Chinese companies, with the remaining spots taken by developers from Japan, South Korea, Israel, Turkey, and others. The direct output from Western developers is relatively scarce on this list, highlighting the regional distribution characteristics of the global mobile game development focus.

It is noteworthy that while Asian developers hold an absolute advantage on the development side, the U.S. market remains the largest revenue source for most top-tier products. Simultaneously, some products primarily targeting the Chinese domestic market successfully made the list based on iOS revenue alone, showcasing the strong spending power of Chinese players.

Product Analysis: Success Factors Focus on IP, Gameplay Fusion, and Cross-Platform Synergy

Looking across the list, successful new releases primarily relied on the following core strategies:

Modern Adaptation and Global Distribution of Classic IPs: Bandai Namco’s SD Gundam G Generation Eternal leveraged the timing of a new Gundam anime release for precise market entry, rapidly achieving $300 million in revenue. Nexon’s Mabinogi Mobile, Netmarble’s Seven Knights Resurrection, and others successfully transformed classic IPs from the PC era into growth drivers in the mobile market. Cygames’ global release of Uma Musume Pretty Derby achieved over $73 million in revenue within six months, proving the global appeal of a quality IP.

“Hybrid Gameplay” Becomes a New Growth Paradigm: This year’s ranking clearly reflects the “hybridization” trend. Century Huatong’s Diandian Interactive’s Kingshot, deeply integrating 4X SLG with tower defense and holiday-themed operations, topped the chart with nearly $586 million in revenue and helped its parent company’s market capitalization exceed 100 billion RMB. Habby’s Archero 2 continued and upgraded the successful formula of Roguelike and hybrid-casual gameplay. Vietnamese Ikame Games’ Screwdom and Turkish Rollic’s Color Block Jam achieved breakout success in the “disassembly” and “color puzzle” genres, respectively, through hybrid IAP and ad monetization models.

Cross-Platform Strategy Amplifies Product Value: Several top products adopted simultaneous or sequential release strategies across PC, console, and mobile. While NetEase’s Where Winds Meet garnered $132 million on mobile, its PC version also quickly attracted millions of players upon its Steam release. Tencent’s Delta Force: Hawk Ops and Valorant: Source both benefited from their PC IP foundations and cross-platform ecosystem synergy, with the latter’s iOS version in China nearing $100 million in revenue in just over three months.

Deep Exploration and Innovation in Niche Genres: Beyond mainstream genres, companies achieved returns by meticulously cultivating specific categories. Playtika’s Disney Solitaire, combining a well-known IP with classic gameplay, became the representative new title in the card game genre this year. Leiting Games’ published Legend of Staff and Sword stood out in the idle RPG track with its unique vertical-screen 2D open world and free class-change gameplay.

Conclusion

The global new mobile game market in 2025, against a backdrop of overall slow growth, exhibited characteristics of “de-unicornization” but “increased diversification.” Asian developers, especially Chinese creators, continue to lead market innovation through more adept IP operation, more flexible gameplay fusion (hybrid-casual/hybrid-monetization), and more determined globalization and cross-platform strategies. Looking ahead, amidst challenges like increasingly scarce player attention and rising development costs, micro-innovations in core gameplay, precise targeting of niche user needs, and leveraging new technologies like AI to improve development and operational efficiency will become key for developers to break through in the new round of competition.

熱門頭條新聞

- Evolution of Game Monetization Maps Global Investment Trends;

- Human Fall Flat Celebrates 10 Year Anniversary Alongside 60 Million Players

- Amazon MGM Studios Unveils Full ‘Warhammer 40,000’ Animated Series Project, Led by Henry Cavill & Blur Studios

- AEVI Releases 2025 Spanish Video Game Report

- The Stone Age Survival Game That Actually Has Color Is Leaving Early Access August 25

- Tiny Teams Festival Returns This August to Celebrate Micro Studios with Massive Ideas

- Two Flagship Industry Reports Unveil Critical Mobile Game Growth Barriers & Winning Strategies for 2026

- London Emerges as Europe’s Undisputed Mobile Gaming Powerhouse