“2025 Global Mobile Internet Industry White Paper” Officially Released: Traffic Dividend Fades, Monetization Capability Becomes Core Competitiveness

Recently, the “2025 Global Mobile Internet Industry White Paper,” co-produced by qimai data, a professional mobile product intelligent business analysis platform, along with Tencent Cloud and ToBid, was officially released. The white paper deeply analyzes the full-year development trends in the mobile app and gaming sectors from a global perspective, aiming to provide developers, promoters, and investors with forward-looking insights and decision-making references.

In 2025, the mobile internet industry demonstrated strong resilience within a complex global economic landscape. However, the industry can no longer easily explain growth through the “traffic dividend” concept. Supply density continues to rise, revenue is highly concentrated among top players, and the success rate of single-path strategies is continually narrowing. In such an environment, monetization capability is no longer just a supplementary phase after product maturity but is becoming a fundamental capability affecting survival and scale.

Global Mobile Ecosystem Overview: User Base Steadily Expands, Competitive Landscape Continues to Evolve

Data from the white paper shows that the global smartphone market maintained positive growth in 2025, with the competitive landscape in the Chinese smartphone market continuously evolving. Global internet usage rates increased steadily, and both the number of Chinese netizens and the internet penetration rate achieved stable growth, providing a solid foundational user base for the mobile internet industry.

Artificial Intelligence: Moving from Technological Exploration to a New Phase of Large-Scale Application

In 2025, artificial intelligence rapidly shifted from the technological exploration phase to a new stage of large-scale application, driving innovation and upgrades across multiple fields.

With the accelerated implementation of AI technology, AI application capabilities are rapidly penetrating from popular tracks like image/video and productivity/office tools into high-value scenarios such as healthcare and more vertical domains. Various AI products are emerging in abundance. Major internet giants are accelerating their C-end AI layouts, with intelligent assistants gradually becoming the core battlefield in the battle for the “super portal.” Simultaneously, these giants are also expanding rapidly into AI hardware, striving to seize the next generation of human-computer interaction portals.

While leading companies continuously expand their AI application territory through “advantage deep cultivation + new domain exploration,” a growing number of small and medium-sized enterprises are successfully breaking through via technological innovation and deep scenario cultivation. Furthermore, the productivity value of AI on the B-side continues to be released, gradually penetrating all aspects of core business operations.

Gaming Industry: Revenue Highly Concentrated, Risk of Single IAP Model Systemically Amplified

From the supply side, the gaming industry remains in a state of high-density competition. The white paper indicates that over 46,000 new games were launched on the App Store in 2025, with more than 20,000 products released in the first half of the year alone. The sustained expansion on the supply side has not slowed down.

However, business outcomes show significant differentiation. According to qimai data statistics, among the Top 1000 iOS games by revenue in 2025, the Top 100 products accounted for approximately 83% of the total revenue, with income highly concentrated among a very small number of top-tier products. This means that under the current structure, a single in-app purchase path is no longer scalable for mass replication. For the vast majority of products in the mid-tier and long tail, business risks are systemically amplified.

In terms of categories, the popularity of shooting games reached a new high in recent years in 2025, and female-oriented games grew rapidly. Mini-programs/games continued their explosive trend, with cross-platform interoperability becoming a key lever for manufacturer growth. At the same time, AI is being integrated and densely implemented across various game production processes; “Gaming+” is opening up new possibilities for industrial development, empowering value growth in multiple fields.

Advertising Monetization: Rewarded Video Becomes a Definitive Anchor

At the level of advertising monetization, the gaming industry shows a highly consistent consensus on monetization – the eCPM of rewarded videos significantly surpasses other advertising formats across different game types. Consequently, advertising has transformed from a “supplementary income source” into a crucial capability for stabilizing the revenue structure.

In casual games, rewarded video impressions do not hold an overwhelming advantage, with structural differentiation appearing across platforms: on the iOS side, banner impressions account for nearly 40%; on the Android side, interstitial impressions take the lead, exceeding 30%. In mid-to-hardcore games, rewarded video holds an absolute leading position on both platforms.

Within the rewarded video format channel, a relatively stable tiered structure has formed among platforms on both iOS and Android. Top-tier platforms form the core主轴, while the second tier maintains a持续 competitive relationship. ToBid maintains a stable share performance in rewarded video formats on both platforms, playing an important role in enhancing efficiency within the game rewarded video monetization structure.

As hybrid monetization becomes the default configuration, game products are beginning to re-evaluate the risks of relying on a single platform. Multi-platform mediation and structural optimization capabilities are becoming key variables in the game monetization system.

Non-Gaming Industry: Free is the Trend, Commercialization Capability Determines Development

Regarding business model structure, free apps remain the absolutely dominant form. Taking apps newly launched and currently available on the App Store in 2025 as examples, free apps account for over 94% in both categories. Looking at the overall structure, more than 80% of existing apps lack the foundational capability for in-app purchases. The industry presents a typical pyramid structure of “a few strongly commercialized products + a large number of weakly commercialized products.” In this context, advertising is not a “supplemental growth strategy” but a fundamental source of revenue.

At the advertising structure level, significant differences emerge across verticals:

AI Tool Products: Ad impressions are highly concentrated in low-intrusive ad formats, with banners accounting for the highest share. However, from a revenue performance perspective, this vertical exhibits monetization characteristics of “low traffic, high premium,” demanding higher ad fill quality.

IoT Products: Heavily reliant on system high-exposure entry points; splash screen ads dominate both revenue and impressions. Rewarded ads find it difficult to generate effective value in IoT scenarios.

Education Apps: Low-intrusive, continuously exposed ad formats are more popular. In terms of impressions, native + banner formats account for over 70%.

Social Products: Native formats hold a significant lead in impressions, but revenue sources show a trend towards diversification.

Overall, there is no single optimal ad format for the non-gaming industry. What truly impacts efficiency is the combination of formats and the ability to match them with specific scenarios. As competition intensifies within vertical apps, running multiple ad formats in parallel is becoming the norm.

Overseas Expansion Achieves Diversified Breakthroughs, Chinese Developers’ Global Map Continues to Expand

In 2025, Chinese developers accelerated their overseas expansion, demonstrating strong strength across multiple tracks.

Short dramas sparked a new wave of overseas expansion, with market size experiencing exponential growth, evolving from an emerging content consumption category into a popular form of mass cultural consumption. Within the short drama赛道, the emerging category of “manhua” (comic dramas) has risen sharply, becoming a new blue ocean for content consumption.

Supported by technological breakthroughs, accumulated experience, and policies, the pace of Chinese AI application overseas expansion accelerated in 2025, becoming a significant force reshaping the global technology landscape. With AI empowerment, cultural加持, cross-platform experience upgrades, and category integration innovation, Chinese games continue to attract overseas players.

Despite the impact of tariff policies, cross-border e-commerce demonstrated strong growth resilience. Besides the aforementioned popular categories, sectors like education, local lifestyle services, and finance are also accelerating their overseas expansion.

##Hot Fields like Micro-Dramas and Local Services Activate New Industry Landscape

The micro-drama market showed an explosive growth trend, having matured from an emerging content consumption category into a popular form of mass cultural consumption, now moving towards a stage of high-quality development.

In 2025, competition in local lifestyle services intensified, extending from scenarios like food delivery to more “people’s livelihood scenarios.” The Internet of Things became a core driver of digital transformation, accelerating its shift from “connectivity” to “empowerment,” with the smart home channel demonstrating strong development momentum.

Cloud Services Market: Moving from “Resource Provision” to “Value Creation”

As the core infrastructure foundation of the mobile internet, the cloud services market is accelerating its shift from “resource provision” to “value creation.” Driven by multiple factors, the scale of the Chinese cloud computing market continues to expand rapidly; cloud service capabilities are upgrading comprehensively and penetrating deeply into thousands of industries. Concurrently, with the rapid development of AI technology, the cloud service industry has completed a rapid iteration from “AI on Cloud” and “AI into Cloud” to “Cloud-AI Integration.”

Traffic Monetization: Moving from Structural Expansion to Efficiency Competition

Focusing on the mobile internet traffic monetization market, the white paper points out that industry competition in 2025 is shifting from “traffic acquisition capability” to “traffic value management capability.” Simply having a full range of ad formats is no longer a competitive advantage. The real gap stems from:

- Multi-platform mediation capability

- Real-time structural optimization capability

- Data transparency and anti-fraud capability

- Stability of rewarded formats and revenue safety margin

For games, this is a guarantee against the risk of relying solely on IAP; for non-gaming apps, this is the foundation for long-term cash flow stability. Traffic monetization is becoming one of the fundamental infrastructures for mobile applications.

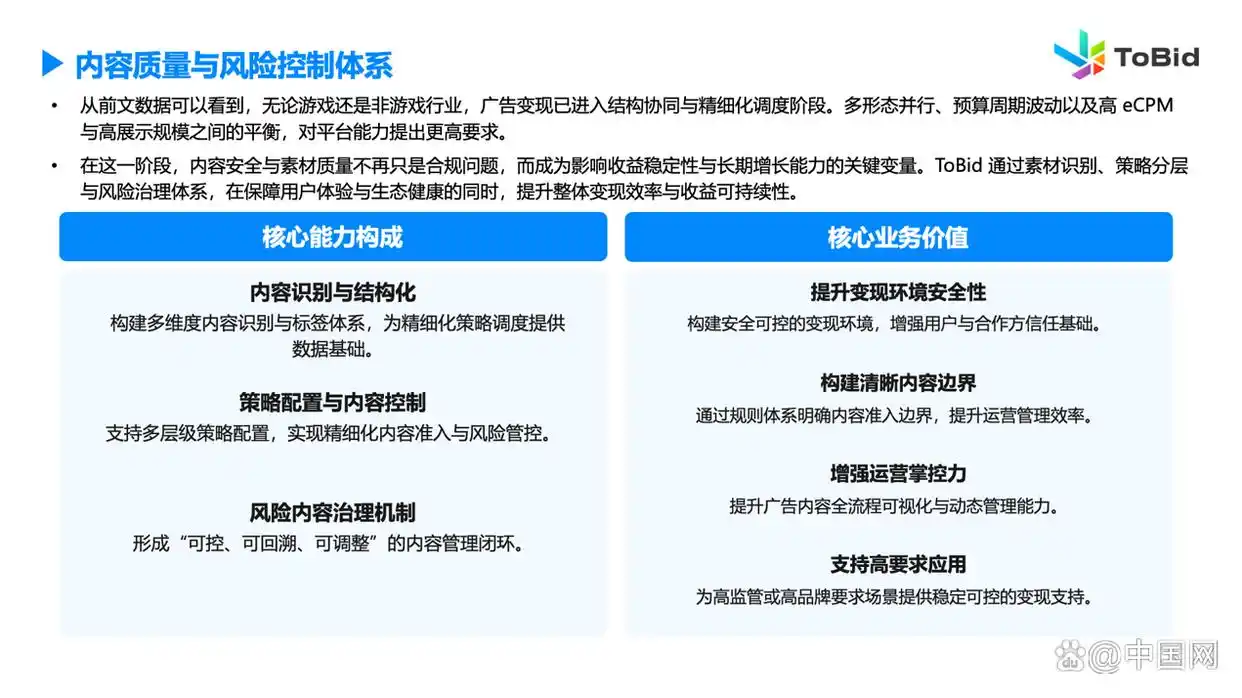

ToBid simultaneously released the “2025 China Mobile Internet Industry Monetization White Paper” based on real monetization data samples, systematically combing the changes in monetization structures and trend judgments for both the gaming and non-gaming industries. As seen in the previous monetization structure analysis, rewarded video has become a core revenue source for both gaming and non-gaming apps. The concentration of high-value formats makes the revenue structure more dependent on this single critical format. In this context, traffic authenticity and data credibility become key variables affecting monetization stability.

When rewarded video becomes a foundational revenue pillar, anti-fraud capability is no longer just a risk control measure but becomes core infrastructure ensuring revenue stability and ecosystem health. To this end, ToBid has constructed a full-link intelligent anti-fraud system for rewarded video, operating multi-layered combination from the terminal, through the data engine, to the server-side, forming a structured protection capability from the bottom up. As ad monetization enters a精细化 stage, data transparency and revenue interpretability become watersheds for platform capability. ToBid achieves full-link traceability and verifiable revenue structure through a three-layer data transparency architecture.

Conclusion: Monetization Capability Becomes Core Determinant of Survival and Scale

In an era characterized by high concentration and high-density supply, monetization capability is no longer an extensive link after product maturity but has become the core capability determining survival and scale. Whoever can complete structural upgrades earlier, and whoever can manage unit traffic value more precisely, will secure more certain revenue space in an increasingly competitive environment.

熱門頭條新聞

- Final Fantasy VII: Ever Crisis to Cease Global Operations This October: Root Causes, Player Impacts and Strategic Adjustments for Square Enix Mobile Business

- Gather Your Blades for August 11 as Swordcery Enters Early AccessHack, slash, and hack again in this roguelite adventure where each sword has a story to tell.

- The 5th KKWORLD KuaiKan Comic Park Takes Place in Guangzhou, Energizing New Vitality for Original Chinese Comic IPs via Immersive Offline Ecosystem

- Stop-Motion Short *Into the Forest* Claims Young Audience Award at Annecy Festival, Elevating Swiss Animation on Global Stage

- Wield magic. Forge friendships. Become a hero in Unicorn Academy: Island of Magic.

- Anthony Neoh: IPO Back on Top Globally, But Sponsor Price Wars Could Hurt Quality

- H1 2026 Chinese Animation Industry Summary: Differentiated Layout Across Platforms, Premium Annual Series Lead Streaming Rankings

- Wuthering Waves Version 3.5 Is Out Now on PC, Mobile, PS5, and Xbox