Driven by Capital Boom and Technological Innovation, China’s Gaming Industry Set to Reach New Heights in 2026

In 2025, the global gaming industry shattered the notion of an “industry downturn” with a record-breaking $161 billion in mergers and acquisitions (M&A). Driven by multi-billion-dollar deals such as Netflix’s acquisition of Warner Bros. Games and the PIF consortium’s leveraged buyout of EA, the industry’s landscape is undergoing profound transformation. Concurrently, China’s gaming market demonstrated robust internal growth and structural optimization, with domestic actual sales revenue exceeding 350 billion yuan and user numbers reaching 683 million. Looking ahead to 2026, with multiple tailwinds including continued capital focus, deeper integration of AI technologies, and the upcoming release of several globally anticipated titles, China’s gaming industry is poised to achieve high-quality development and enhance its global influence, building upon a solid foundation.

- Capital Boom: Record Global M&A, Strategic Investment Becomes Main Theme

According to the latest Drake Star report, global gaming M&A transaction value reached $161 billion in 2025, with just two deals – Netflix’s acquisition of Warner Bros. Games ($82.7 billion) and the PIF consortium’s acquisition of EA ($55 billion) – contributing over $100 billion. Capital allocation trends were distinct:

Strategic M&A Leads: Deep integration between media and gaming, with leading companies strengthening ecosystem positioning through acquisitions.

AI and Mobile Sectors Favored: AI companies focusing on transforming game production, such as Luma AI and General Intuition, secured significant funding; in mobile gaming, Dream Games received a $2.5 billion investment, while casual and social sub-sectors remained active.

Strong Public Market Performance: The Drake Star Gaming Index rose 12% annually, with companies like Unity and NetEase seeing significant stock price increases.

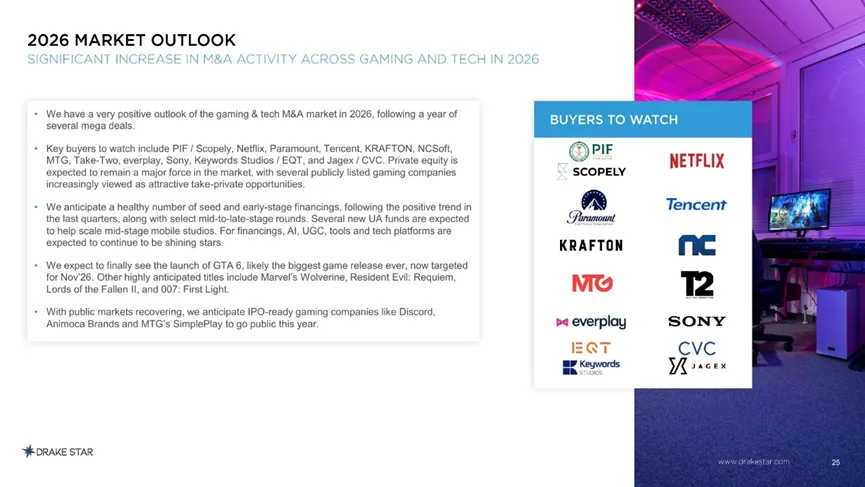

This trend is expected to continue into 2026, with potential revival in the IPO market (companies like Discord and Animoca Brands may list) and possible increased privatization of listed gaming companies by private equity.

- The Chinese Market: Structural Optimization, Steady Growth, and “Gaming Economy” Ecosystem Emerges

The 2025 China Gaming Industry Reportindicates China’s gaming market exhibited “simultaneous growth in volume and quality” in 2025:

Revenue and Users Hit New Highs: Domestic actual sales revenue reached 350.789 billion yuan, a year-on-year increase of 7.68%; user base reached 683 million.

Highlights in Sub-sectors: Client game revenue grew 14.97% year-on-year; the console game market saw explosive growth of 86.33%, reflecting rising player demand for high-quality experiences; mini-program games continued their explosive growth, with market scale reaching 53.535 billion yuan (up 38.56% year-on-year), becoming the industry’s “second growth curve.”

“Gaming Economy” Ecosystem Scale Emerges: The total economic scale directly and indirectly driven by gaming was estimated for the first time to exceed 12 trillion yuan, forming a multi-layered value circle radiating from gaming to hardware, esports, IP derivatives, and cultural tourism integration.

III. Globalization Deepens: From “Product Export” to “Cultural Resonance”

In 2025, the actual overseas sales revenue of China’s self-developed games reached $20.455 billion, a year-on-year increase of 10.23%. The US, Japan, and South Korea remained the primary markets, collectively contributing nearly 60% of revenue. In terms of product types, strategy games (including SLG) accounted for nearly 50% of the top 100 overseas revenue-generating self-developed mobile games, demonstrating the sustained advantage of Chinese companies in this genre.

The industry is transitioning from “product globalization” to “cultural globalization,” seeking deeper emotional connection and cultural resonance with global players through in-depth localization, IP integration, and technological empowerment.

- 2026 Outlook: Triple Drivers – Technology, Products, and Ecosystem

Deep Empowerment by AI Technology: AI applications in content generation, operational optimization, and user experience personalization will mature further, driving production process transformation and cost efficiency.

Global Blockbusters Drive Market Heat: The release of super titles like GTA 6 (expected November 2026) is anticipated to ignite global player enthusiasm, boosting hardware sales, streaming ecosystems, and related derivative consumption.

Deep Integration with the Real Economy: The “Gaming+” model will continue to expand, creating new scenarios in cultural tourism experiences, urban renewal, educational applications, and other fields, amplifying the industry’s spillover value.

Improvement of Regulatory and Compliance Systems: As the industry’s scale and social influence grow, establishing robust systems for minor protection, content review, and data security will become the cornerstone for healthy industry development.The strong influx of global capital in 2025 and the steady growth of the Chinese market have laid a solid foundation for the further development of the gaming industry in 2026. Facing a new phase of accelerating technological iteration, diversifying player demands, and deepening global competition, China’s gaming industry needs to further strengthen its capabilities in content innovation, independent R&D of technology, and ecosystem building to seize opportunities in the continuously heating global market and achieve a leap from “scale leadership” to “value leadership.”

(Data Sources: Drake Star’s Global Gaming Industry Investment and Financing Report 2025; China Audio-Video and Digital Publishing Association’s China Gaming Industry Report 2025)

熱門頭條新聞

- The gaming universe is in motion. And not in just one direction.

- EU Allocates €6.1 Million to Empower Game Studios for Innovative Tools & New Business Models

- Insight ’26: The Post-Production and VFX Business Conference

- gamescom 2026: Games spark excitement for the future

- SIGGRAPH 2026 Unites Global Computer Graphics Community in Los Angeles With Landmark Keynotes, Inaugural Games Summit, and AI Innovation

- Deck-Building Roguelike Adventure Talespinner Comes to PC & Switch This August

- Full Event Lineup Unveiled for PIS 2026, The 27th Preview in SEOUL Builds Integrated Global Textile Industry Platform

- Google to Open Google Play to Third-Party App Stores Starting Last Week ; Antitrust Ruling Reshapes Android Ecosystem with Short-Term Revenue Pressure on Google