China and USA: the World’s Two Largest Digital Economies

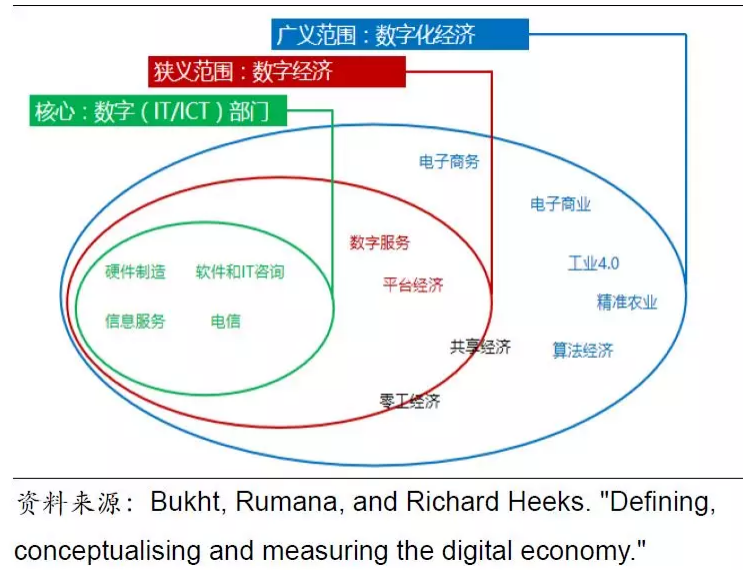

The triple division of the digital economy: The core is ICT (Information and Communications Technology). The second level is the narrow sense of digital economy, which mainly refers to the new business model brought by the application of data and data technology. It highlights platform business model like e-commerce, which also includes “share economy” and “zero economy”, traditional business model changing to platform model. But digitalization involves every level of the economy, from manufacturing to traditional stores, everyone needs application of digital and information technology. The third level is the broad definition of digital economy, which involves almost all economic activities.

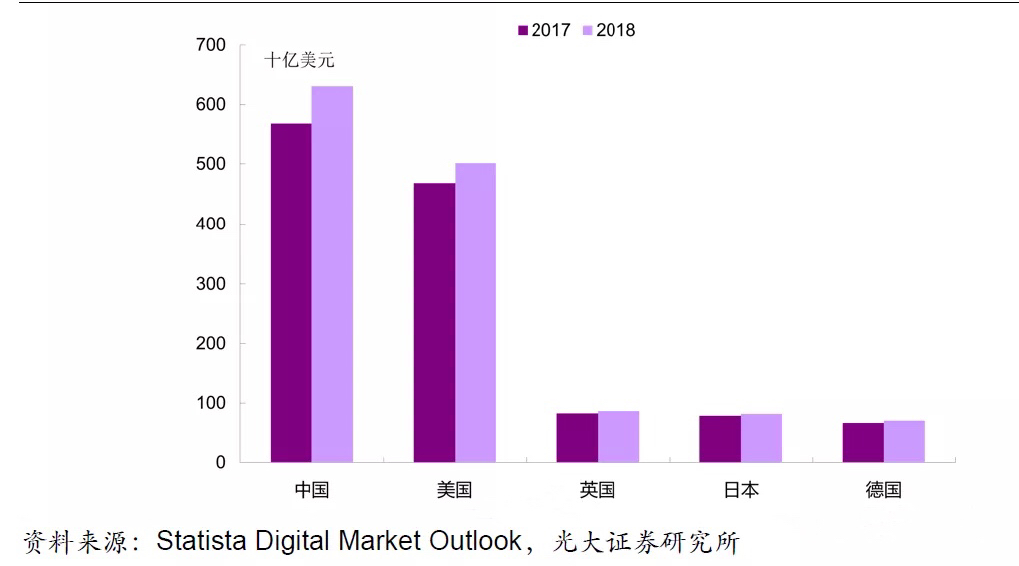

A representative indicator is that the size of the e-commerce market in China and the United States is far ahead. In terms of market capitalization, among the biggest 7 global platforms, Tencent and Ali are from China, with the rest from US, Europe and Japan all falling behind. The new pattern of global competition in the digital economy model is being reshaped. So, are the two big digital economies the same? When it comes to digital economy, the idea of artificial intelligence, machine substitution, automation, etc. always refers to machine replacing labor. Many people worry about damages to workers. The model of digital economy development between China and the United States has commonalities and also significant differences. General speaking, America’s digital economy favors capital, is capital-friendly, and China’s digital economy leans more to labor, more labor-friendly than the U.S.

The size of the e-commerce market in major countries

U.S.: Capital-biased Digital Economy

The scale effect of digital economy increases efficiency, which should be reflected in labor productivity. But the growth rate of US labor productivity has slowed down in the last 10 years.

There are several possible explanations. One is that overall labor productivity is offset by other factors, such as the long-term unemployment caused by the great recession after the financial crisis reduces workers’ skills for a period of time. Second, errors in national income statistics, such as the underestimation of intangible asset investment, leads to the underestimation of output (GDP). Third, the time gap. It takes time for the expansion of general purpose technology to penetrate into all levels of the economy.

The new business model of the digital economy brings economies of scale and increases industry concentration while increasing efficiency, such as the platform economy built by Internet giants, patent ownership, data monopoly and so on. The use of intangible assets and big data leads to industry concentration. Not only in new economic mode, even in the field of traditional businesses, industry concentration pressure is increasing. Eg. online price comparison leads to goods and services becoming more and more transparent, so that efficient enterprises win, inefficient enterprises exit. Maintaining inefficient operations using opaque pricing is becoming more and more difficult.

From the perspective of digital economy, American technological progress is more capital-oriented and capital-friendly. On one hand, industry concentration increases, monopoly rent increases the rate of return on capital. On the other, routine work is replaced by machines, and workers’ pay is squeezed. There is a special phenomenon in the era of digital economy called “star economy”. The star economy can be enterprises or individuals. The use of digital technology enables star companies and individuals to serve large markets at low cost, a few people and the enterprise winner-takes-all, and returns on intangible assets rise.

China: A Labor-biased Digital Economy

Compared with the United States, China’s several relevant indicators show: first, China’s industry concentration has also risen, especially in the past couple years. You may immediately associate the increase in industry concentration brought about by supply structural reform and cutting capacity, but that mainly involves heavy industry and upstream industries. In the past few years, not only concentration in manufacturing but also service industry, including wholesale and retail industry, has been rising, which is a reflection of the scale effect of the development of digital economy.

In contrast to the USA, China’s share of wages has risen over the past decade and its return on capital has fallen. It is worth mentioning that the data of labor remuneration ratio comes from the Bureau of Statistics, which is the statistical caliber of national income, which is conceptually consistent with the labor remuneration ratio in the United States. The decline in the rate of return on capital is consistent with the logic of the increase in the proportion of labor remuneration, which reflects the relationship between capital and labor in the distribution of income.

In summary, the difference between China and the United States in the development of digital economy, lies mainly in the population density and labor costs, which makes technological progress in the United States more labor substitution, and in China, more labor complementary. Some of America’s replacement jobs are regular manufacturing lines, and China is more of a regular worker, such as takeaways, couriers, delivery men, drivers and so on. China has the largest number of platform economies in the world. According to statistics in 2015, 64 of the 175 global platforms valued at more than US$1 billion were from China.

Source: Everbright securities strategy meeting

熱門頭條新聞

- The 2025 3D Creative Talent Showcase Competition is coming with a bang!

- CGGE Signs Memorandum of Understanding with Future Design School of Harbin Institute of Technology

- Exploring the China-U.S. Gaming Dynamics

- The Future of Animation

- Game of Thrones: Kingsroad Launches on Steam Early Access

- 2025 (Beijing) InfoComm China

- Once Human Mobile Launch Set for April 23

- NVIDIA Blackwell Ultra for the Era of AI Reasoning